On February 9, while doing research on something else, I noticed that Harlequin’s Author Solutions, Inc.-run self-publishing imprint, Dellarte Press, had closed its doors. Dellarte’s website is now a placeholder, with a “we’re sorry” message.

Some of you may remember the outcry that greeted Dellarte (originally named Harlequin Horizons) when ASI and Harlequin rolled it out in November 2009. (By contrast, the earlier launch of WestBow Press for Thomas Nelson caused barely a ripple). Writers flipped out. A slew of pro writers’ groups either issued statements condemning the move or de-listing Harlequin. Ultimately, the bad press forced Harlequin to change the service’s name and also to distance itself from Dellarte. Of the several self-pub divisions run by ASI for traditional publishers, Dellarte was the only one that didn’t prominently tout the connection with its parent publisher.

Why such an abrupt, unannounced closure for Dellarte? Harlequin hasn’t talked, and neither has ASI. But maybe it was because Dellarte did almost no business.

Mick Rooney, writing about the closure in The Independent Publishing Magazine, discovered that over the past 5 years, Dellarte published just 16 titles. This is a shockingly small number, and understandably, some people were skeptical, including Nate Hoffelder of The Digital Reader*. However, it’s been confirmed for me by an independent source (and also by the report I discuss below).

The question that immediately occurred to me: is Dellarte an exception? Or are other ASI imprints also doing tiny business?

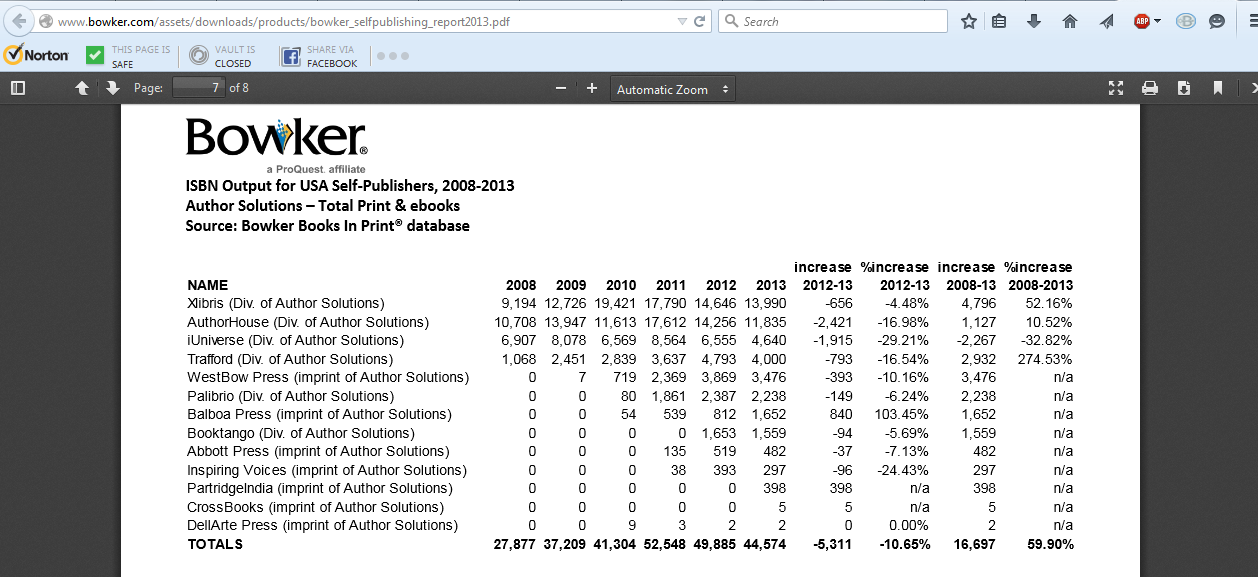

The answer is “not really.” A report by Bowker, Self-Publishing in the United States, 2008-2013, includes a special section on total print and ebook ISBN output at ASI**, which indicates that production at most ASI imprints is in the four-figure range. However, only Xlibris and AuthorHouse crack five figures. And the statistics show something even more interesting: production at ASI is in decline.

There’s an up-and-down pattern for individual imprints, but overall, ASI production increased steadily between 2008 and 2011, when output hit a high of 52,648. (Though compare that to CreateSpace’s 2011 ISBN output of 58,862.)

In 2012, things started to slip. Numbers rose at Trafford, WestBow, and Palibrio, but fell at other imprints (Xlibris and AuthorHouse by around 3,000 ISBNs each); as a result, overall output declined to 49,885. (For the same period, CreateSpace output more than doubled, to 131,460.)

The slide accelerated in 2013. With the exception of Balboa Press and Partridge India (which Bowker only started tracking that year), every single ASI imprint lost ground. Total output fell to 44,574, a decrease of 5,311. Meanwhile, CreateSpace continued its meteoric rise, leaping to 186,926.

We’ll have to wait for 2014 stats to know whether this trend will continue, but my guess is that it will. In part, ASI is reaping the fruits of its poor reputation and the large amount of negative publicity and commentary it has received in the past few years (see, for instance, David Gaughran’s The Case Against Author Solutions). Beyond that, though, I think that its business model–print-centric, high-priced, with outsourced operations (much of ASI is based in the Philippines) and an extreme emphasis on upselling–is simply becoming less and less relevant in this age of free-to-cheap digital self-publishing solutions.***

———————————-

* Nate suggested that the number was so small because Dellarte titles have been folded in among other ASI imprints. But ASI has always been very careful to preserve the division between its own operations and the imprints it runs for others, and does everything possible to distance itself (for some of the imprints, you have to look at the Privacy Policy to know that ASI is involved). It has also kept Abbot Press running and separate, even after Writer’s Digest bowed out. So I think it’s unlikely that it made Dellarte titles disappear.

** Archway Press is not included because Bowker did not start tracking it until 2014. Many thanks to David Gaughran for sharing this report with me.

*** Other companies featured on this blog that lost ground in 2013: PublishAmerica, Dorrance, and, surprisingly, Smashwords (though overall, Smashwords’ output is second only to CreateSpace’s; the decline could also reflect fewer authors choosing to use ISBNs).

David,

I hate to sound cynical, but I think that Harlequin and Random were both special circumstances that would be hard to repeat.

In the case of Random and Hydra, it was a combination of direct involvement by SFWA's then-president, and Random House being unusually sensitive to criticism. If John Scalzi hadn't picked up on my blog post about Hydra on his hugely popular blog, I doubt anyone would have taken notice; and if it had been a different publishing house, they might just have hunkered down and let the storm blow over. (At the time, based on the advances Hydra was paying, most Hydra authors wouldn't have qualified for SFWA membership anyway, so the threat of de-listing by SFWA wasn't as powerful as it might otherwise have been.)

With Harlequin, I think the situation was unique because of the genre focus. It was the outcry in the romance community, which is incredibly protective of its genre, that drove the reaction. RWA issued a statement, which created a domino effect of other writers' organizations weighing in. Harlequin was also uniquely vulnerable because romance is all it does; it needs the approval of the romance community far more than Random House needed the approval of the SF community. So writers' groups had much more leverage than they would have with, say, Hachette.

I was glad of the reaction, but also found it really frustrating, given that WestBow Press, which had been rolled out only weeks before, not only didn't spark any protest but actually got approving nods from some in the industry. And the third-party imprints that have been launched since then–Balboa Press, Abbott Press, Archway Press (which did prompt some criticism, mainly because of its sky-high prices, but no real protest), and the Partridges–have barely even been noticed, except by ASI watchers like you and me.

I do think that the Dellarte debacle is why ASI never again tried to create a genre-specific imprint. So it had that effect. But I'm really not sure that writers groups have the will to oppose ASI, especially with all the other urgent issues facing them these days. I would like to be wrong, though, and I wouldn't be opposed to trying.

I visit a lot of writing blogs and professional sites since I do a weekly blog listing useful writing articles and news items important to working writers.

Because of this, the Google ads, etc., I get are skewed toward various writing scams and overpriced publishing services.

A vast majority of these ads are for self-publishing services which suggests, not only are these services being more aggressive in going after the naive, but that the perceived path to being publishing for most new writers is self-publishing, not a paper book in a bookstore from a "real" publisher.

Victoria:

Do you think there is any chance of getting the same coalition of writers' orgs together on this issue? It was so effective in 2009, and again in 2013 with Random House and Hydra/Flirt. Although if memory serves it took the threat of delisting Harlequin/Random as qualifying markets. I wonder if the various writers' orgs would be willing to come together and do something similar on this.

I get that it's trickier now, with PRH's ownership and the large number of partnering publishers, but isn't it worth trying?

Things have changed.

D2D does seem to have the advantage, only because they provide a better author interface, reporting, and payment.

The word is out on AS, and many Indies would rather pull their teeth with pliers than do anything with them. They are nothing more than garbage.

Self-publishing is no longer a dirty word. Quality reads continue to excite the marketplace, and the authors who care about their readers lead the way.

You are three steps behind this new reality. No more rose-colored glasses. Get with it or shut up.

Smashwords also allows use of non-Smashword ISBNs. http://www.smashwords.com/about/supportfaq#isbn

But I think Smashwords may not be pertinent in this discussion if the primary focus is the print market. They don't offer a print option for their books. Authors/small presses will have to use Createspace or Lulu for print editions in addition to Smashwords for ebook distribution.

Re: authors using their own ISBNs–I thought of that too, after I published my post. Also, I imagine that plenty of Lulu authors don't use ISBNs at all. By contrast, ASI _only_ puts out titles with ISBNs. So the stats in the Bowker report are a real picture of the ASI's production, whereas Lulu and CreateSpace have production that the report doesn't pick up at all. Which puts ASI even farther behind the top 3 providers.

Victoria,

The one other caveat I would add to the Bowker ISBN figures is that even with the downturn in ASI output, it doesn't take into account the bucket load of authors using CreateSpace and Lulu using their own ISBNs. Whereas authors caught in the ASI net are locked into using the various imprint ISBNs. I think the only reason ASI is still maintaining so many of its own print-centric imprints is because it helps to muddy the water for newbie authors who don't realise an imprint is run by ASI.

This is great news.

I too was going to suggest that Smashwords may be losing some ground to D2D.

I haven't heard much about Draft2Digital, but Mick Rooney of The Independent Publishing Magazine gives it high marks.

The fact that Smashwords loses ground can also be caused by Draft2Digital which has garnered better reputation (more modern/fast etc.) and seems to have more appeal for Self-Published authors